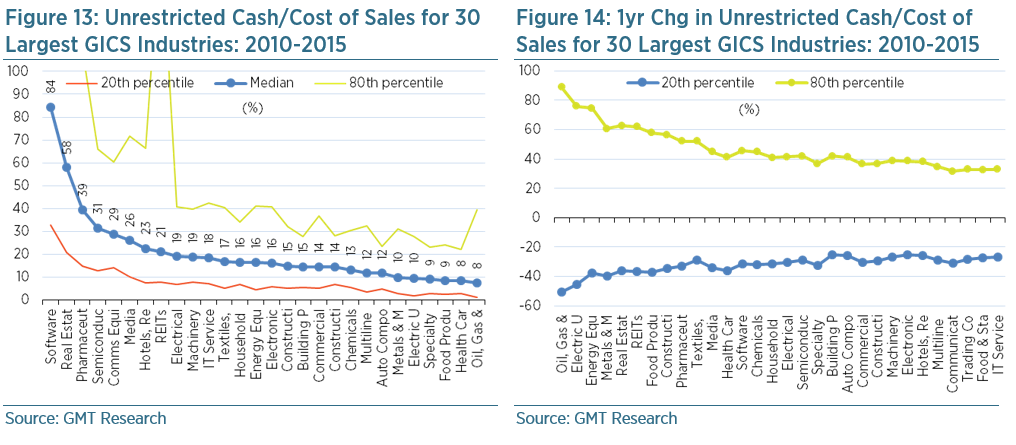

We penalise companies with extreme levels of unrestricted cash relative to their cost of sales (i.e. cash is too high or too low relative to cost of sales). This is a liquidity red flag for working capital requirements. Unrestricted cash funds working capital which eventually converts into cost of sales. Small amounts of unrestricted cash may indicate that a company has problems funding its working capital. At the opposite end of the spectrum there may be instances where the company has very large amounts of unrestricted cash but still feels the need to raise cash or borrow money. This suggests the cash may be fake, or is restricted and used for undisclosed loans.

There is considerable difference in the level of cash relative to cost of sales. In general, high margin business models with better terms of trade (i.e. receive cash early in the service delivery process) have larger levels of cash relative to cost off sales, as shown in Figure 13.

Under our accounting screen a red flag is triggered when cash/cost of sales is below the 20th percentile or above the 80th relative to industry peers (i.e. it is either very high or very low). Red flags are also triggered when cash/cost of sales changes at an unusually large rate over 1 and 3 years. Again, this is when the increase is below the 20th percentile relative to industry peers between 2010 and 2015, or the drop exceeds the 80th percentile.

Under our accounting screen a red flag is triggered when cash/cost of sales is below the 20th percentile or above the 80th relative to industry peers (i.e. it is either very high or very low). Red flags are also triggered when cash/cost of sales changes at an unusually large rate over 1 and 3 years. Again, this is when the increase is below the 20th percentile relative to industry peers between 2010 and 2015, or the drop exceeds the 80th percentile.