We penalise companies with a high and/or rising level of inventory relative industry peers. For the purposes of our analysis, we have used two ratios: inventories as a percentage of sales and of cost of goods sold. The reason we include both is that some companies are not required to report their cost of goods sold and so the more traditional inventory days metric fails to populate. Additionally, there is no established definition of cost of goods sold meaning that comparisons can be misleading. There are a number of reasons to be concerned about inventories:

- Obsolete inventory and future impairments: Most products have a limited life-span and decline in value over time. Persistently large inventories of finished goods might represent unsold and outdated products which should be written-off. Alternatively, large inventories could reflect inefficient management of the manufacturing process.

- Deteriorating future profitability: Rising levels of inventory could simply reflect a company which is ramping up a new production line. If this is the case, it should be a temporary phenomenon. Alternatively, rising inventories might reflect deteriorating margins, thereby increasing the numerator relative to the denominator. More commonly, rising inventories reflect increasing input costs which will translate into falling future margins and lower profitability.

The amount of inventory a company maintains is generally defined by its business model. Business models with lower inventory are generally (but not always) regarded as being better than those with higher levels. Warehousing and organising inventory consumes resources, both management and financial. After all, both the warehouse and the inventory need to be financed which reduces profitability.

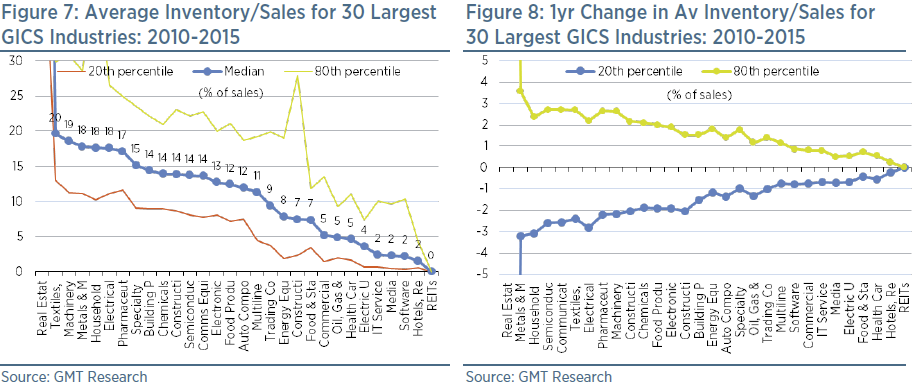

The real estate development sector has the highest level of inventory with a median average of 158% between 2010 and 2015. Thereafter, it is the textile and machinery sectors in a very distant second and third place, as Figure 7 shows. Hotels, media and IT services have the lowest level of inventory. Most sectors maintain inventory levels at between 10-20% of sales.

Sectors with the largest inventories are generally those that experience the greatest volatility; as such, the real estate developers often see their inventories fluctuate by 40% of sales (150-odd days) in any given year. Most other sectors see volatility of 1-3% (4-11 days) of sales in any given year.

There’s not that much difference in the level of inventory held by different countries, although China had by far the highest level of all major markets at a median average of 17% of sales (62 days) between 2010 and 2015. This compares to just 10% of sales (37 days) at US companies. One of the reasons for such a high level of inventory in China is that VAT is due within a few weeks of issuing an invoice; however, the tax can be offset by inventory purchases. As such, companies carry more inventory than necessary in order to minimise their tax bills.

Our accounting screen is set to trigger a red flag when inventory/sales exceeds the 80th percentile (i.e. it is very high) relative to GICS industry peers, and/or when there is an abnormally large inventory build-up relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the deterioration in inventory exceeds the 80th percentile relative to the change experienced by industry peers between 2010 and 2015.