We penalise companies with a high and rising level of capitalised interest relative to pre-tax profit. While there is some logic to the concept of capitalised interest owing to timing differences, the level of interest capitalised can be subjective and used to manipulate reported profits. Also, capitalised interest can lead to companies with identical assets booking different values on these owing to the amount of interest capitalised.

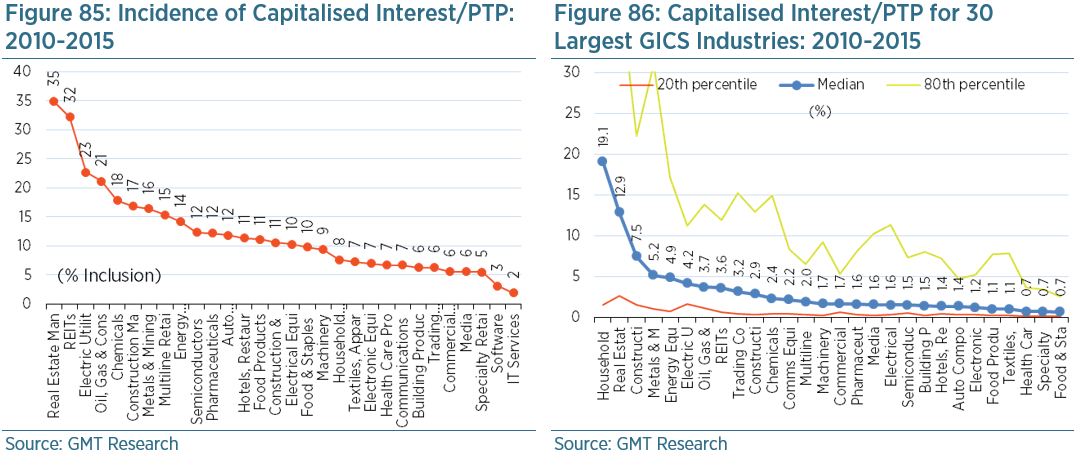

Around 11% of all companies in our global sample of 16,000 capitalised interest although the amounts were generally fairly small at a median average of 3% of pre-tax profit. As Figure 85 shows, asset-heavy sectors, such as real estate, electric utility and oil & gas, are most likely to capitalise interest. Meanwhile, asset-light sectors, such as IT services and software, are the least likely to capitalise interest. Unsurprisingly, capitalised interest is also most meaningful in asset-heavy industries, as shown in Figure 86.

Our accounting screen is set to trigger a red flag when capitalised interest/pre-tax profit is in the highest 80th percentile relative to GICS industry peers (i.e. it is very high), and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in capitalised interest/pre-tax profit exceeds the 80th percentile relative to the change experienced by global peers between 2010 and 2015.