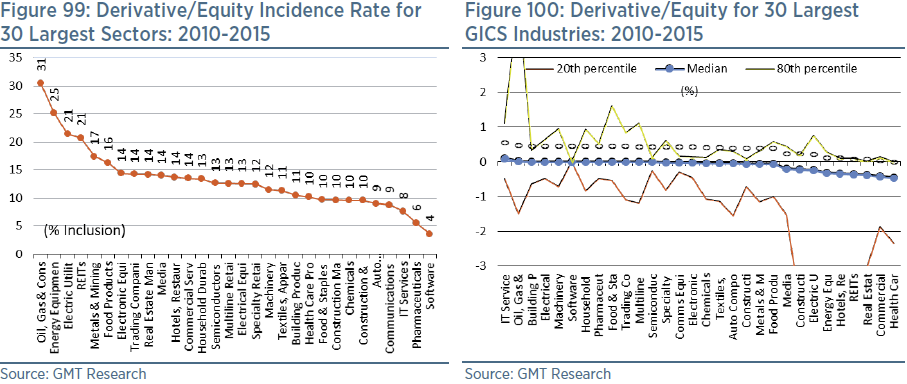

We penalise companies with a high and/or rising exposure to derivative and hedging assets. According to Bloomberg, just 14% of companies disclose data on their net derivative positions, with the highest inclusion rate being commodity related sectors, such as Oil & Gas, as shown in Figure 99. In many instances, derivatives are used to remove risk from the business but sometimes large exposure is a sign that a company has taken a speculative view on a financial asset, such as commodities or currencies. Furthermore, included in this balance sheet classification might be the present value of future estimated cash flows, used to inflate the profits of companies such as Enron (ENRNQ US) in 2000 and Noble Group (NOBL SP) in 2013. As Figure 100 shows, most companies have net derivative exposure of less than 1% of equity.

Our accounting screen is set to trigger a red flag when derivatives exceed 10% of equity, and/or when there is an abnormally large increase relative to the normal rate of change amongst global peers over one and three years. This latter red flag is triggered when the increase in derivatives to equity exceeds the 80th percentile relative to the change experienced by GICS industry peers between 2010 and 2015.