Intangible assets include goodwill, patents, copyrights, trademarks, trade names, organization costs, capitalized development costs and software, franchises, licenses, property rights, core deposit intangibles (banks), and intangible portion of prepaid pensions.

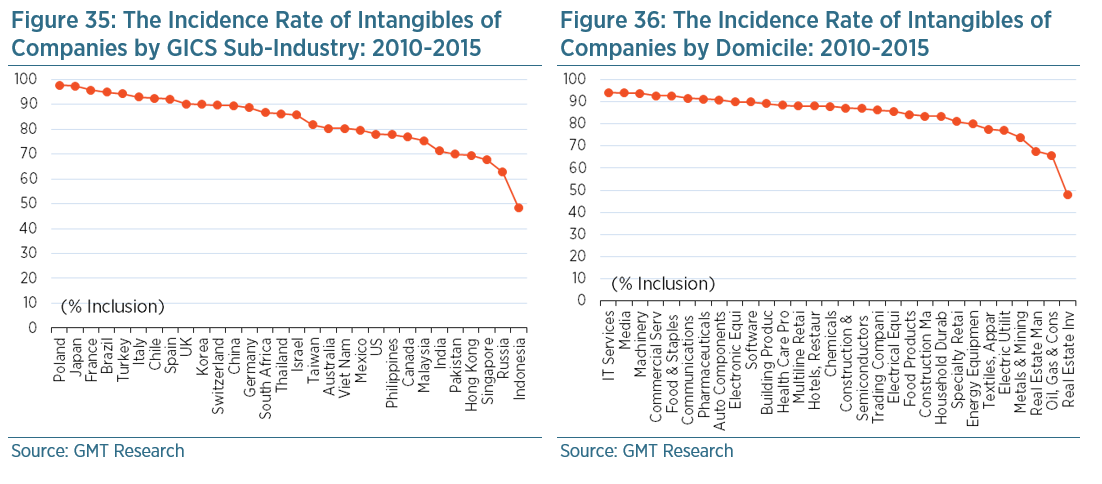

We penalise companies with large and/or rising intangibles relative to industry peers. More than 80% of the 16,000 companies in our sample have some form of intangible asset on their balance sheets. As Figure 35 shows, intangibles are far more likely to be found within people-orientated businesses, such as media and I.T., than on capital intensive ones, such as real estate and oil & gas. Within capital intensive industries, investors are buying tangible assets, such as mines and property, as opposed to people and brands. There is quite a difference in intangibles by domicile, as Figure 36 shows; however, it’s not immediately clear why. Russia and Indonesia have noticeably lower exposure to intangibles. This might be because they are resource rich countries where acquisitions are fairly uncommon (please refer to the flag on Acquisitions & Disposals for more information).

While most companies might have some intangibles on their balance sheet, it is usually small, equating to less than 5% of sales, as Figure 37 shows. Media and software companies have the largest amounts of intangibles, which is to be expected, in excess of 10% of sales. Meanwhile, domiciles with the largest amounts of intangibles are generally developed markets, such as the UK and the US, where intangibles exceed 15% of sales. In these markets there is a culture of acquisitions and disposals which combined with a knowledge-based economy (as opposed to a resource-based one) create the pre-requisite environment for the creation of intangibles.

Valuing intangibles, such as goodwill, brand value and intellectual property, leaves a lot of room for discretion. In general, we are concerned with companies that have generated a large and growing amount of intangibles as it suggests growth is being pursued through acquisitions. Some intangibles represent licence or concession fees. As long as the operator obeys the terms of the agreement, a valuation based on cost which is reduced over time seems reasonable. However, it is more subjective valuing goodwill created through acquisitions. We would be especially concerned when acquisitions have been followed by material downward revisions to profit forecasts as it suggests that a future impairment is possible.

Our accounting screen is set to trigger a red flag when intangibles/sales exceeds the 80th percentile (i.e. they are very high) relative to GICS industry peers, and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in intangibles to sales exceeds the 80th percentile relative to the change experienced by industry peers between 2010 and 2015.