We penalise companies that cede a large percentage of their profits away to minority investors in their subsidiaries on the basis that debt can sometimes be made to look like a minority interest. We also penalise companies where minorities account for an increasing portion of pre-tax profits.

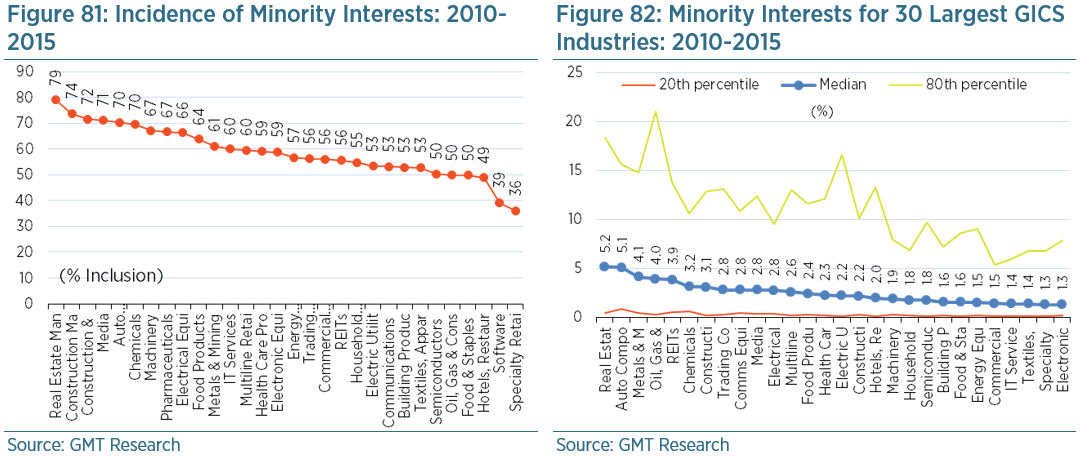

Just over half of all companies in our global sample of 16,000 report a minority interest of some form, although these are relatively small with a median average of 2.4% of pre-tax profit. Real estate companies are most likely to have minority interests with an incidence rate of 79%, and these are likely to be the most material at 5% of pre-tax profit. Speciality retail is the sector least likely to have minority interests.

Our accounting screen is set to trigger a red flag when minority interest/pre-tax profit exceeds the 80th percentile (i.e. it is very high) relative to global peers, and/or when there is an abnormally large increase relative to the normal rate of change amongst global peers over one and three years. This latter red flag is triggered when the increase in minority interest/pre-tax profit exceeds the 80th percentile relative to the change experienced by global peers between 2010 and 2015.