A minority interest, which is also referred to as non-controlling interest (NCI), is ownership of less than 50% of a company's equity by an investor or another company. For accounting purposes, minority interest is a fractional share of a company amounting to less than 50% of the voting shares.

We penalise companies where minority interest account for a material and/or rising portion of net assets relative to global peers. As discussed in our report, CHINESE PROPERTY DEVELOPERS: Weak Foundations (13 July 2016), it is possible to structure financing from trusts (and other sources) as equity. In simple terms, a trust company buys a minority shareholding in a subsidiary company which the controlling company buys back at a later date at a higher price; the difference represents the investment return. While this might meet the accounting criteria for equity, in substance it is debt. As such, we penalise companies where equity accounts for a large share of total equity.

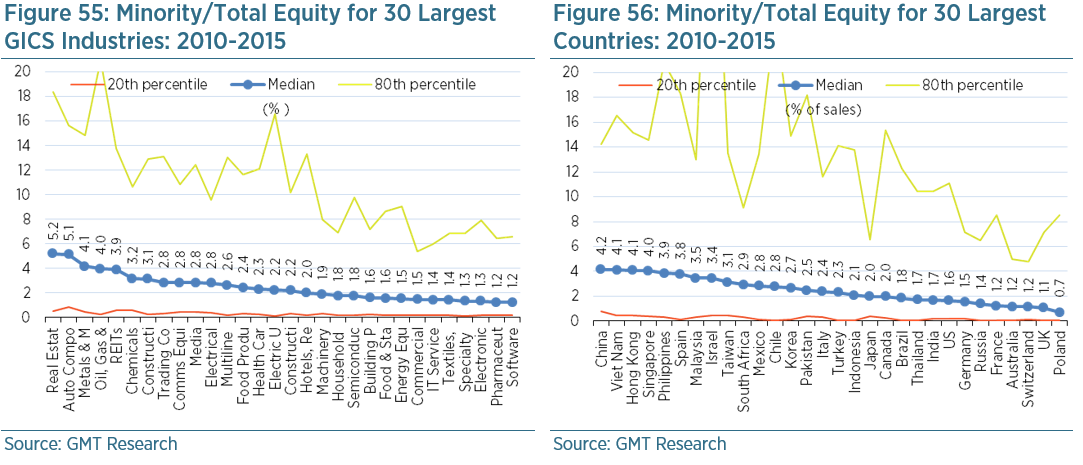

Around 59% of all companies report minority interests although these tend to be quite small at just 2.4% of total equity. There’s huge variance in the incidence of minorities by country, as Figure 53 shows. In markets like Chile, China and France, more than 80% of listed companies report minority interests whereas it is less than 50% in places like the UK, US and Russia. There is less variance by industry, as Figure 54 shows. The real estate developers would appear to have the highest incidence at 80%.

Our accounting screen is set to trigger a red flag when minority interests/total equity exceeds the 80th percentile relative to our global sample, and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in minority interests/total equity exceeds the 80th percentile relative to the change experienced by the global sample between 2010 and 2015.