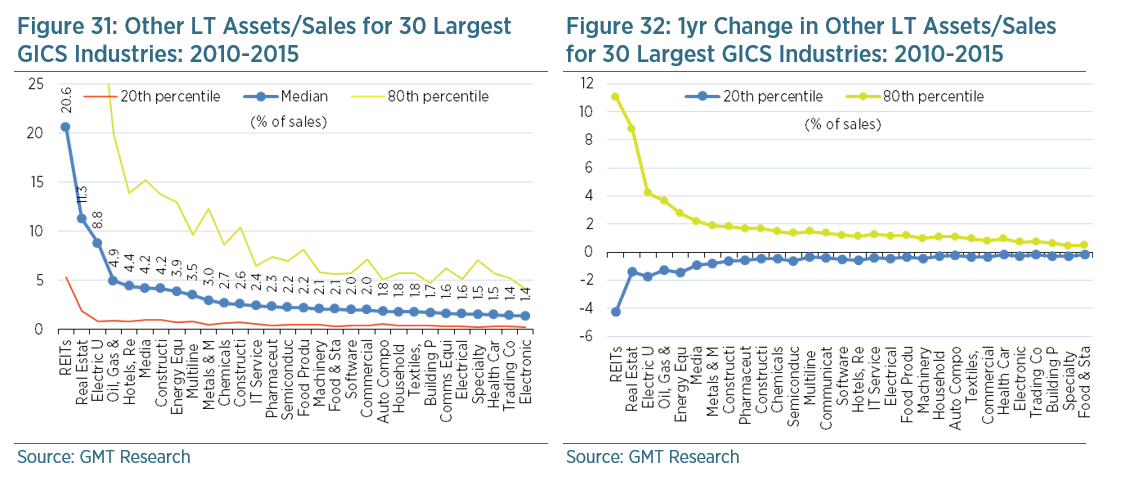

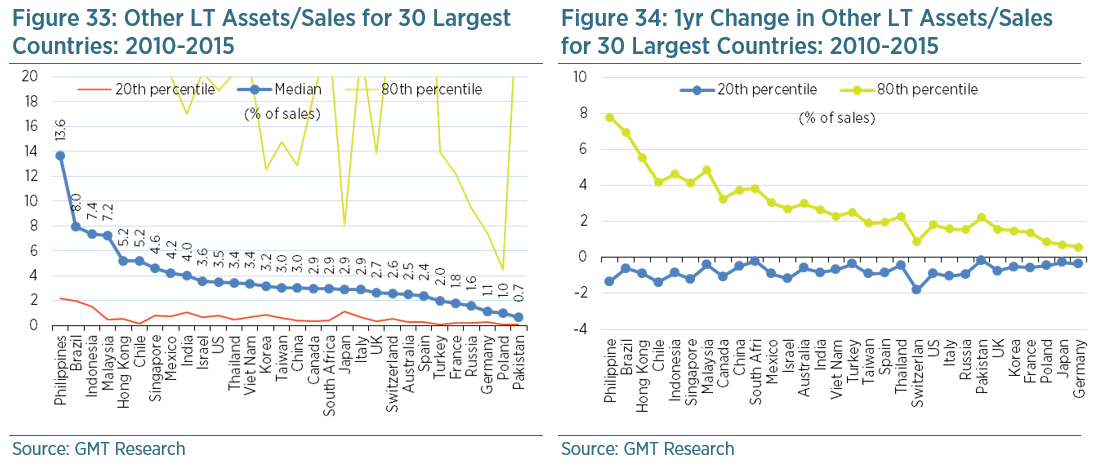

Includes all other long-term assets that have not already been included as fixed assets, long-term investments & receivables, deferred tax assets or intangibles. Commonly includes investment in affiliates, other receivables, derivative & hedging assets, prepaid pension costs or long term assets of discontinued operations. We penalise companies with a high and/or rising level of other long term assets relative to industry peers. Other long term assets are normally a fairly small balance sheet item, typically accounting for less than 5% of sales whether it is by sector (Figure 31) or country (Figure 32). The exceptions are the real estate sectors (developers and REITS) where other long tem assets account for more than 10% of sales. These tend to include other long term receivables, advances and investments in associates. The Philippines appears to have unusually high exposure to other long term assets but this would be due to the classification limitations of Bloomberg. Conglomerates with property divisions tend to have their investment property assets classified as other long term assets.

Non-traditional assets, such as overdue receivables and loans which management might not want to write-down, often end up here. Investors should be concerned with large or increasing balances. Given that this is generally a small balance sheet item, it tends not to fluctuate by more than 1-2% of sales, as Figure 32 shows.

As these assets are long term in nature, they will be matched by movements in the financing or investment portion of the cash flow statement. As such, companies could theoretically make a long term loan, or advance, to a customer who in reality is unable to pay. This would enable the company to continue reporting strong profits and operating cash flow while maintaining receivables at a normal level. This is known as “round tripping”. For more information please read our report CURIOUS ASSETS: And dubious Profits (11 Feb 2015)

Our accounting screen is set to trigger a red flag when other long term asset/sales exceeds the 80th percentile (i.e. they are very high) relative to GICS industry peers, and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in other long term asset/sales exceeds the 80th percentile relative to the change experienced by industry peers between 2010 and 2015.