We penalise companies with a high level of prepaid expenses/inventory relative to industry peers. Prepayments are commonly used as deposits for construction-in-progress or for the acquisition of future inventory. They are an area of auditing vulnerability because they can also be used to remove fake cash from the balance sheet. In reality, this cash might have been stolen by management or never have actually existed (having been created through illusionary profits from scams such as round-tripping).

Auditor verification is limited to confirmation that the payment has been made, not what it is actually used for. In many cases, advance payments make little sense, especially for inventory. The usual excuse given by management is that they wish to beat future inflationary rises of supplier stock, to lock in a secure supply of inventory, or that suppliers find it difficult to borrow money from banks.

Excessive prepayments for inventory may be a red flag when the company already has large amounts of inventory in place. Prepayments also represent a credit risk with suppliers since the company is effectively lending money to them. Why are banks not willing to lend to these suppliers instead? Is the company actually subsidizing suppliers so they supply cheaper products that enable the company to report artificially low cost of sales? Why does the company trust these suppliers so much to trust them with large cash prepayments? Is this is a sign they are undisclosed related third parties?

The incidence of prepayments is relatively low, with 22% of the 16,000 companies in our sample reporting some. Of these, the median average prepayment was just 10% of inventory, rising to 57% for the 80th percentile. Prepayments are more likely to be found in hotel, food staples and speciality retail sectors, as shown in Figure 117. There is also considerable difference by country, with 70% of all companies in Vietnam reporting prepayments, as shown in Figure 118.

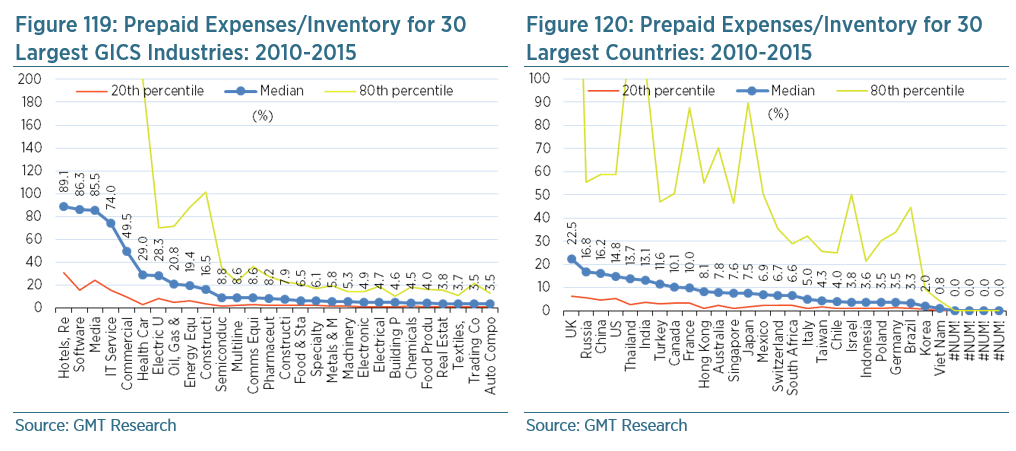

Prepayments are most likely to be material in those sectors with low inventories, such as hotel, software and media companies, as shown Figure 119. For most industries, prepayments account for less than 10% of inventories. Interestingly, while Chinese corporates have a reputation for reporting a large number of prepayments, in reality only 29% of companies have issued them. However, a median average of 16% of inventory is pretty meaningful, as shown in Figure 120.

Our accounting screen is set to trigger a red flag when prepaid expenses/inventory is in the highest 80th percentile relative to GICS industry peers (i.e. it is very high), and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in prepaid expense/inventory is in the 80th percentile relative to the change experienced by industry peers between 2010 and 2015.