We penalise companies with a high and/or rising level of short term debt as a percentage of total debt relative to industry peers. Companies which are reliant on short term funding are more vulnerable to liquidity shocks than those with longer-term debt finance as debt facilities can be withdrawn immediately. While companies with short term financing are likely to have a lower cost of debt than those with longer-term financing, should interest rates rise, those with short term financing will see rates rise faster.

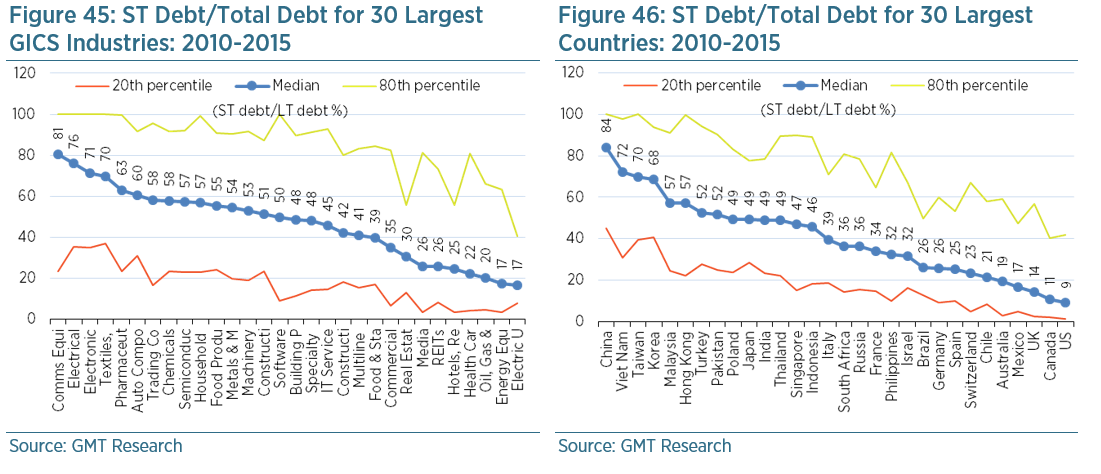

In general, industries with longer investment lead times, such as electric utilities and oil & gas, rely on longer-term financing. Short term debt typically accounts for less than 25% of their total debt, as shown in Figure 45. Meanwhile, general manufacturing industries have far greater exposure to short term debt where it typically accounts for more than two thirds of their total debt. Interestingly, emerging markets tend to have a far greater reliance on short term debt for their funding needs than developed ones, as shown in Figure 46. We suspect that this is a corporate governance issue. Companies in emerging markets, such as China and Vietnam, are far more opportunistic when it comes to running their balance sheets and less aware of the dangers of funding long term assets with short term funding.

Our accounting screen is set to trigger a red flag when short term debt/total debt exceeds 60% of total debt (i.e. the 62nd percentile) relative to all global companies, and/or when there is an abnormally large increase relative to the normal rate of change amongst global peers over one and three years. This latter red flag is triggered when the increase in short term debt/total debt exceeds the 80th percentile relative to the change experienced by global peers between 2010 and 2015.