In another theme, we decided to detail every related party transaction across ASEAN and Hong Kong. After all, every accounting shenanigan that we’ve written on includes related party transactions. Alarmingly, we found that 95% of all companies were engaged in related party transactions across pretty much every market. While many of these could be explained away in ASEAN, it was clear that the Chinese companies listed in Hong Kong were up to all sorts of antics. Companies were sourcing materials from the founder, lending money to and from associates in order to flatter profits, and so on. For more details, read our report RELATED PARTY TRANSACTIONS: Family Games in HK and SG (23 Feb).

If you’re not yet convinced that something’s wrong with China’s corporate sector, take a look at our report on government subsidies, BENEFITS STREET: Subsidies to Chinese companies are ballooning (8 Sept). We found that a 98% of all Chinese companies had some form of direct subsidy and that for 20% of all companies this exceeded 20% of profit. We made no attempt to quantify the impact of hidden subsidies such as cheap electricity, loans or land but these could be even more material. Chinese returns on equity are already some of the lowest in Asia. One shudders what returns would be without subsidies.

But why are accounting shenanigans so common in China? Part of the reason could be down to leverage. The Chinese corporate sector is the third most highly leveraged globally, as highlighted in our recent report, GLOBAL EVALUATION: Suspended Disbelief (13 Oct). Leverage creates a need for business owners to meet the expectations of outside interests, such as bankers, in order to ensure the supply of credit continues. As such, this creates an incentive to aggressively recognise sales, manufacture cash flow and create fictitious profits from related parties.

Despite our findings, the sell-side remains resolutely optimistic on Chinese companies. Around 79% of all analyst recommendations on Chinese domiciled companies(1) are Buys, compared to 54% globally. If we strip out overseas listings and focus on A-Shares (domestically listed companies), this percentage rises to 88%, the highest globally. Of the 7,400 analyst recommendations on companies where there are more than three analyst recommendations, there are just 286 sell recommendations….that’s less than 4% of all recommendations.

Given this supposedly bullish sentiment, it’s perhaps no surprise that China’s stock market valuations are demanding. In fact, the median trailing price earnings ratio (PER) of Chinese domiciled companies is 39x. As the chart below shows, this makes Chinese companies the most expensive in the world…by far. India is the second most expensive on 26x. This PER multiple rises to 48x if we only include A-Shares! We prefer to use a median multiple as opposed to a weighted index multiple because indices are often distorted by one or two large companies.

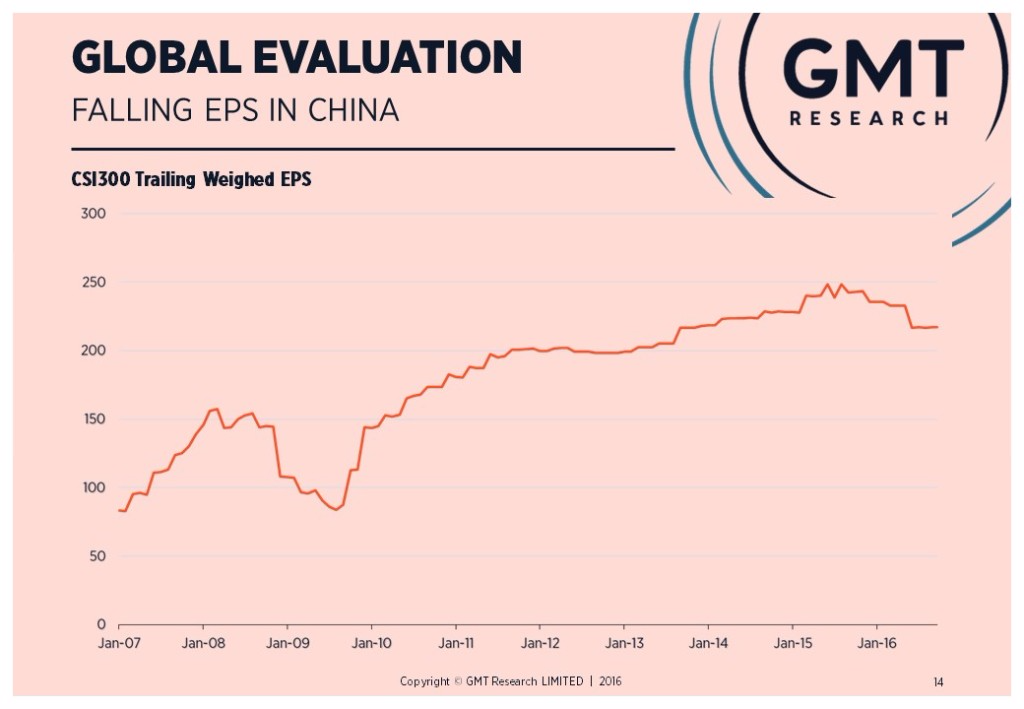

Given demanding valuations, you would expect Chinese corporate profits to be rising at a brisk pace, but no, they’re falling. Weighted average EPS for the CSI300 peaked in August 2015, and is now down around 11% YoY. Given that its over-leveraged corporate sector is still generating free cash outflows, capex will have to fall further in order for companies to begin the long de-leveraging process. That means EPS will fall further.

So how can analysts be so positive on one of the world’s most expensive stock markets when EPS is falling, companies are over-leveraged and accounting is questionable? Well, part of this optimism is due to the conflicts of interest inherent in the broking system and part is just naivety; however, intimidation also seems to have played an important role. There have been widespread reports that analysts, traders and brokers have been arrested by the authorities(2). Indeed, the government was reported to be actively supporting the stock market again after the panic sell-off earlier this year(3).

Arresting stock brokers and analysts is equivalent to shooting the messenger. Some of us remember the last time a government tried this – back in Southeast Asia in the lead up to the 1997 Asian Financial Crisis. It smacks of desperation. A free market is just a pricing system which tells you where to allocate resources. China’s quasi-nationalisation of its stock market seems to be because it doesn’t like the message. Maybe the government should shut it down instead. After all, it’s going to cause them a lot more embarrassment in the near future given leverage, the direction of earnings and valuations. We would expect the main stock market indices to more than halve from here. Sell and/or short.

1. For companies with more than 3 analyst recommendations.

2. http://www.telegraph.co.uk/finance/china-business/11835412/China-cracksdown-on-market-rumours-with-mass-arrests.html

http://www.cnbc.com/2015/09/01/in-chinas-fixed-market-rule-breakers-are-probed.html

3. http://uk.businessinsider.com/china-is-intervening-in-its-stock-market-through-direct-buying-and-banning-short-sales-2016-1