A deferred tax liability results from a temporary timing difference between the company's accounting and tax carrying values, the anticipated and enacted income tax rate, and estimated taxes payable for the current year.

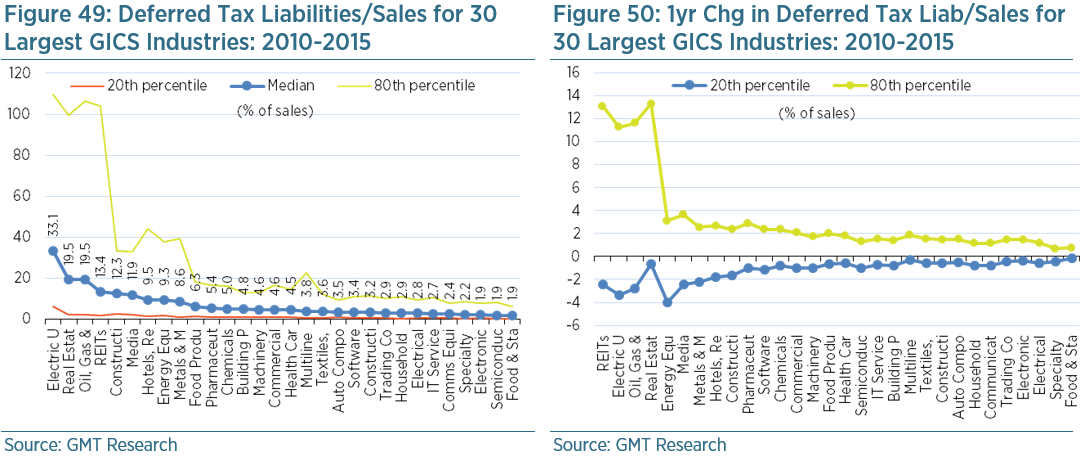

We penalise companies with large and/or growing deferred tax liabilities relative to industry peers. Deferred tax liabilities are commonly found in capital intensive industries, such as electricity utilities, where fixed assets are depreciated at a faster rate for tax purposes than to shareholders, as shown in Figure 49. As such, profit and tax reported to shareholders is larger than reported to tax authorities in the earlier stages of the asset’s life. It should be stressed that the amount of tax paid over the asset’s life will remain the same.

Deferred tax liabilities are also created when companies revalue their assets, such as the property sector. They can also be commonly found by highly acquisitive companies that revalue some of their newly acquired assets. If a company revalued an asset by US$100m, it would create a theoretical tax liability equivalent to the effective tax rate. Assuming that rate is 25%, the deferred tax liability would be US$25m. The company would report a net revaluation gain of US$75m though the income statement and establish a deferred tax liability of US$25m on the balance sheet. If the company went on to sell that asset for US$100m, the deferred tax liability would be reduced to zero and there would be no impact on the income statement.

Deferred tax assets are also commonly found in companies that use financial asset modelling, such as the wastewater treatment and waste-to-energy sectors in China. Under financial asset modelling, companies estimate the returns they will generate over the life of the concession (revenues received less capex and operating expenses. These are then amortised fairly evenly over the life of that concession for reporting purposes. As such, reported profits are generally higher than they would be in the earlier stages of the concession and lower in the latter stages. The authorities do not recognise financial asset modelling for tax purposes and, as such, concessionaires pay tax according to intangible asset modelling i.e. the asset is capitalised and then amortised over the life of the concession. Because profits reported to shareholders are far higher than that reported to the tax authorities in the earlier stages of the concession, a deferred tax liability is created. Clearly, financial asset modelling is highly subjective and open to abuse. For further reading on deferred tax liabilities please refer to our report, PROFIT MANIPULATION: Deferred Tax Liabilities (30 April 2014).

We would be especially concerned about substantial deferred tax liabilities being found in industries where they were not expected or an abnormally large build-up in industries where they were expected. As such, our accounting screen is set to trigger a red flag when deferred tax liabilities/sales exceeds the 80th percentile relative to GICS industry peers, and/or when there is an abnormally large increase relative to the normal rate of change amongst industry peers over one and three years. This latter red flag is triggered when the increase in deferred tax liabilities/sales exceeds the 80th percentile relative to the change experienced by GICS industry peers between 2010 and 2015.