A gardening company

CGBG is basically a fancy gardening company although the official definition goes something like this: “an integrated landscape architecture design service provider, offering a one-stop solution which includes design and planning, design refinement, construction, seedling cultivation and maintenance.”

Arguably, should not be listed

Gardening companies have no fixed assets, only their employees. As such, we would question whether they should become listed companies. Indeed, while 14 gardening companies are listed in China, there are none outside. We suspect the reason they’ve listed in China is that the outsized Chinese property bubble has created a temporary boom in the need for landscape gardening. This will one day pass, as will likely their profits. Indeed, CGBG clearly states in its prospectus[1] that revenues are “not recurring in nature” (Page 6) and that they are reliant on property developers or local governments for all of their business (Page 144).

Relies on just two customers

CGBG would appear to have little bargaining power owing to an increasingly concentrated customer list. In 2013, 45% of revenue was sourced from smaller customers individually accounting for less than 10% of sales; however, this had fallen to just 16% by 2016. Indeed, two customers accounted for 81% and 84% of total sales in 2015 and 2016, respectively, although the two largest ones in 2016 were both new.

A highly competitive industry

There are thousands of landscape gardening companies in China, as you would expect from a highly commoditised business with low barriers to entry. Indeed, an IPSOS survey conducted for CGBG’s IPO estimated that there were over 17,000 landscape architecture services providers in China with 1,200 providers focused on landscape design services (Page 73 IPO Prospectus). The top ten landscape architecture service providers had less than a 5% market share of revenues. And this is where things start to get a little bizarre….

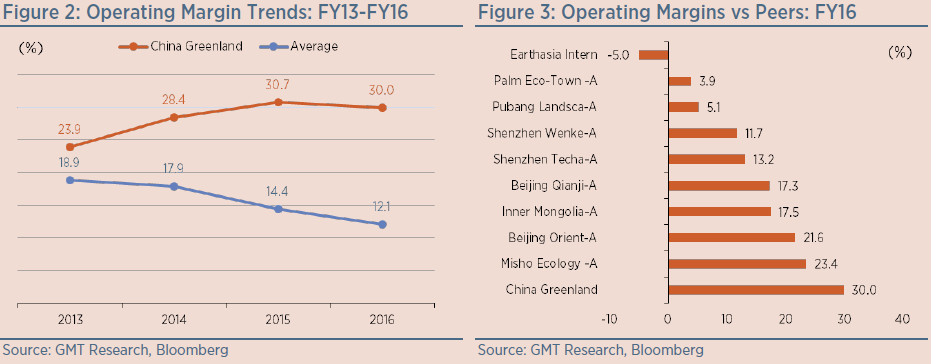

Whopping margins

You would have thought that operating in a highly commoditized and competitive sector would lead to razor thin margins; but no, CGBG’s operating margin came in at a whopping 30% in 2016. Not only that, its margin has risen by 602bp since 2013, whereas its closest competitors have recorded an average deterioration of 677bp over the same period (we have excluded recent listings).

Inconsistent story

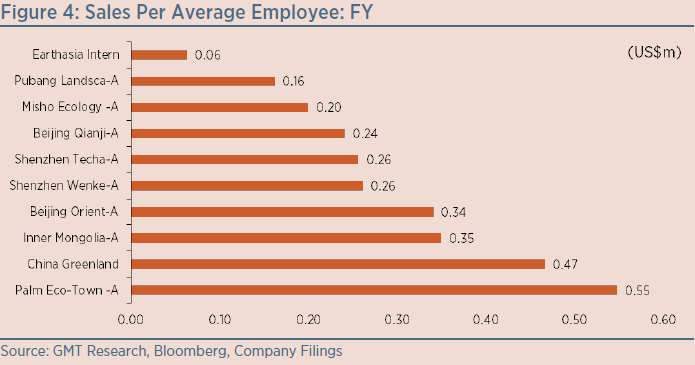

CGBG claims its superior margins are due to limited subcontracting; however, in its IPO prospectus, the company stated that it outsourced all its construction work and general gardening to subcontractors (Page 5). Furthermore, if CGBG had brought subcontracted work back in-house, this should be reflected in lower sales per employee relative to peers; however, sales per employee of US$0.47m is double the average of its peers. Also, while sales per average employee fell 7% in 2016, its operating margin was broadly unchanged. In short, the company’s explanation does not add up.

Subjective accounting and dubious profits

We are concerned that CGBG’s profitability stems from its highly subjective accounting which gives management enormous scope in determining profits. For example, the company had unbilled receivables of 402 days in 2016 – that’s revenues which it recognises but has yet to actually bill the client for. It has a further 245 days of trade receivables – revenues which have been billed for but the client has not yet paid. In total, it takes 647 days to get paid. While the magnitude of these metrics are not entirely unusual compared to its peers (although definitely at the long end), the rate of increase in receivables has far outstripped its peers over the last few years. Total receivables increased by 193 days in 2016 alone. In fact, the RMB545m increase in receivables equated to 75% of sales which suggests that cash revenues received were just 25% of reported sales.

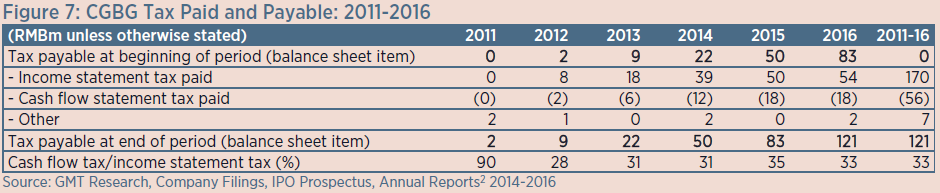

Confirmed by a lack of tax payment

If a company has not billed for work done, it doesn’t want to be paying taxes on these sales and profits. Indeed, CGBG’s cash flow tax paid averaged just 33% of its income statement tax recognised between 2011 and 2016. In other words, it is accruing for tax but not reporting it to the tax authorities or paying it. Instead, tax accumulates as a payable on its balance sheet. This amounted to RMB121m by end-2016 which, assuming a 25% corporate tax rate, implies profits recognised but not yet billed of RMB484m – that’s 96% of CGBG’s entire profit history! Either CGBG is being overly aggressively in recognising its revenues or it’s been unable to get projects signed-off in order to issue an invoice.

Unrealistic forecasts

Despite missing sales and profit forecasts by 25% and 20%, respectively, in 2016, CGBG has issued[2] highly aggressive future guidance with sales forecast to rise by 581% between 2016 and 2019, and profits by 395%, justified by a five-fold increase in its order backlog since 2014, to RMB3.7bn by end-2016. Even if we give the company the benefit of doubt over its sales forecast, its forecast profit numbers cannot be achieved. Forecast 2019 sales of RMB4.9bn imply receivables of close to RMB10bn based on current payment terms, and likely more if the deterioration continues. This needs to be financed. Assuming a third of this is debt financed (and in reality, far more is likely), interest expenses would rise to around RMB212m, 6x higher than forecast and shaving 21% off profit. There would also likely be significant EPS dilution through successive rounds of capital increases. The numbers are simply too good to be true.

Inability to secure long-term funding

As CGBG’s receivables have ballooned, operating cash outflows have accelerated. Although receivables appear to be long-term and have an implicit government guarantee, the company has financed them with RMB405m of expensive short-term debt costing 8.1%, of which 79% is off-shore (US$ and HKD). Total debt equated to 62% of equity by end-2016. It would have made more sense to finance receivables with cheaper, on-shore debt, if it was available. As such, CGBG’s financing structure makes little sense.

Chairman has pledged shares for a company loan

In order to secure a RMB138m credit facility for CGBG, Chairman Wu Zhengping and his wife have pledged 330m. Both Huishan and Hanergy displayed unusual trading patterns. In the six months prior to Hanergy’s suspension, the 20-day moving average Bid or Ask volumes were greater than 60% of total volumes for 14% of the time (volumes should be split pretty evenly between the Bid and Ask), and over 50% of the time at Huishan. By comparison, the 20-day moving average Bid or Ask volumes for CGBG have exceeded 60% of total volumes for over 95% of the time over the past six months. Most of these volumes are on the Ask which suggests someone may be trying to push up its share price.

More shares might be pledged

We are concerned that a significantly larger proportion of the founder’s shares may have been pledged but this need not be disclosed under Rule 13.17 of the Listing Rules. Hong Kong’s Central Clearing And Settlement System (CCASS) details shares moving onto its system and then into brokers’ accounts. While the system would not show who has put up a stock as collateral, it’s likely to be a result of margin financing by a controlling shareholder. The information showed that the number CGBG’s shares held in the system to be 1.4bn at the end of September 2016, 42% of the total. Assuming a free-float of 31% plus the known pledged shares equating to 9.9% and we arrive at an expected total of 41%, roughly the same as that disclosed. However, by the 28th March 2017, a further 624m shares were in the system, equating to 19% of the company. Have these shares also been pledged? We do not know.

Conflicting signals

CGBG is an oddity. At face value, it appears to be enormously profitable (judging by its margins) with great prospects (according to its own guidance). However, a number of issues don’t make sense: widening margins have bucked industry trends, it does not seem to be getting paid (as evidenced by deteriorating receivables) and pays almost no tax (which suggests real profits are far smaller than reported). There is also cause for alarm in that a significant number of pledged shares along with highly subjective accounting gives a motive and means of inflating profit, while unusual trading patterns suggest that the stock is being supported.

Follow the founder

We don’t think CGBG’s future is nearly as bright as its management would have us believe. Future profit forecasts cannot be met under its current capital structure and, even then, the property bubble will come to an end one day. Perhaps that’s why CGBG’s founder has sold down his stake, disposing of 30% to Greenland Holdings (600606 CH), a mainland Chinese property developer, in February 2017[6]. This leaves him with a 30% direct stake. On 35x trailing PER and 7x price to book for a gardening company, he’s laughing all the way to the bank!

Reference:

[1] Global Offering, 30 June 2014

[2] Corporate presentation, March 2017; CBGB Annual Reports 2014, 2015, 2016.

[3] HKEx: Pledging of Shares and Charge over Account by Controlling Shareholder, 25 April 2017

[4] Financial Times: Hanergy secured $200m loan ahead of solar group stock tumble, 25 March 2015; Financial Times: Hanergy founder Li Hejun spent $50m on more stock on crash day, 27 May 2015

[5] Financial Times: Ping An, Far East Horizon clarify exposures after Huishan Dairy price plunge, 27 March 2017

[6] HKEx: Completion of Change in Shareholding, 27 Feb 2017