A foreword

You probably can’t remember why you subscribed to this newsletter, and I wouldn’t blame you; we’ve been remiss in maintaining it. In case you’ve forgotten, GMT Research is a Hong Kong-based accounting research firm that advises fund managers on accounting shenanigans at listed companies across Asia. You may have come across us when one our past exposés hit the headlines, including Noble Group (delisted), AirAsia (delisted), CK Hutch (1 HK), CIMIC (delisted), Treasury Wine (TWE AU), and Evergrande (delisted), to name a few[1].

You could be forgiven for thinking that we’d closed shop given our lack of recent communication, but we’ve been busy behind the scenes – just a little less publicly than before. We’ve identified a number of bagels (and near-bagels) well ahead of share price collapses, including China Tianrui (1252 HK), Energy Absolute (EA TB), Fullshare (607 HK) and many more[2]. Furthermore, our Accounting Watchlist – a shortlist of large Asian companies with accounting issues – underperformed local benchmarks by 20ppts over 2025. In other words, it’s generally not good news if we’re talking about a company.

We’ve tried various iterations of this newsletter - mostly involving outside contributors - but haven’t yet found a format that works. After a bit of a rethink, we’ve decided to bring it back in-house. Every few months, one of us will pen a short missive focusing on a topic of interest arising from our recent research. For this newsletter, we thought to highlight data centre operator GDS…

Do Data Centres Earn Their Keep?

GDS's FY25 results were broadly as expected. Revenue and adjusted EBITDA both rose 11% year-on-year. Operating profit before long-lived asset impairments improved 31% to RMB1.5bn, helped by the low prior-year base. Guidance for FY26 was also roughly in line with expectations, with management pointing to revenue growth of around 9-13% and adjusted EBITDA growth of around 6-11%. At the income statement level, therefore, performance appeared encouraging.

The more interesting issue is what those numbers say about returns. GDS is an extremely capital-intensive business. It builds or leases data centre capacity, fills it with equipment, signs customers, and then earns revenue over time. This is an asset-heavy infrastructure model, which means the quality of the business should be judged mainly by whether the assets earn a return above their cost of capital.

The business should be judged mainly by whether the assets earn a return above their cost of capital

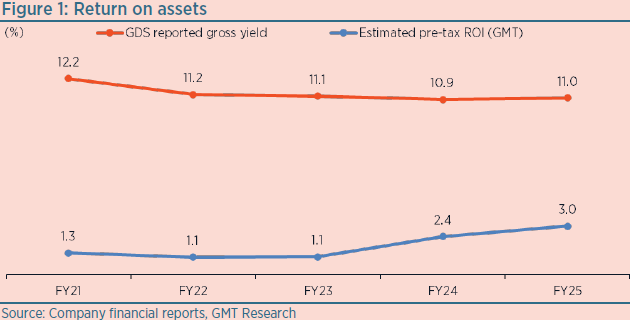

On that basis, the picture remains underwhelming. We estimate that GDS’ China business generates a pre-tax return on operating assets of only around 3%. That is below its cost of net debt, which we estimate at roughly 4.9%. Put simply, the assets do not appear to be earning enough.

Management presents the economics more favourably by highlighting what it calls adjusted gross profit yield. This measure takes adjusted gross profit and divides it by gross property, plant and equipment, excluding construction in progress. In FY25, this produced a yield of around 11%. At first glance, that sounds respectable. It suggests GDS is earning a double-digit cash return on its completed data centres.

However, the metric is flattering. The biggest problem is that adjusted gross profit excludes the cost of depreciation. For some companies, depreciation can be a notional accounting charge that may not say much about underlying economics. For data centres, it matters a lot. GDS’ assets have finite useful lives. Much of the asset base consists of data centre equipment, leasehold improvements and leased assets, with useful lives commonly measured in years rather than decades. Servers, power systems, cooling equipment and fit-outs do not last forever. They have to be maintained, replaced and upgraded. In that context, depreciation is not an optional accounting measure. It is part of the cost of doing business.

GDS excludes the cost of depreciation when calculating gross profit yields, but it is part of the cost of doing business

The second issue is the denominator. GDS’ yield calculation uses gross PP&E excluding construction in progress. We think that is too narrow. A more sensible measure of capital employed should include the net book value of operating PP&E, right-of-use assets, goodwill and other intangibles. These are all part of the capital committed to the business. Once we compare GAAP gross profit with this broader operating asset base, the return falls sharply. In FY25, the gross profit yield was around 5.4%. After deducting other operating costs, the pre-tax return was only about 3.0%, as shown in Figure 1, and the post-tax return was closer to 2.4%.

That is a very different story from the 11% figure. One version says the assets are producing healthy cash returns. The other says they are barely covering, or failing to cover, the cost of funding. The difference comes down to whether we treat depreciation and the full asset base as real economic costs. We think investors should.

We estimate a gross profit yield of around 5.4%, approximately half the 11% GDS provides

There are also some accounting details worth watching. GDS’ depreciation rate has been drifting lower. Depreciation and amortisation allocated to cost of revenues was 6.0% of gross PP&E in FY25, down from 6.6% in FY21. That decline is a little odd because the asset mix appears to have moved towards data centre equipment, which should generally have shorter useful lives than buildings. All else equal, that should push depreciation rates up, not down.

One possible explanation is the large impairment charges taken at the end of FY23 and in FY25. GDS recorded RMB4.0bn of PP&E impairments, followed by a lower depreciation charge thereafter. If short-lived assets were impaired, future depreciation would fall, mechanically lifting reported profit in later years. That does not necessarily mean anything improper has happened. Impairments can be entirely legitimate. But it does mean that current returns may look slightly better than the underlying economics would otherwise suggest.

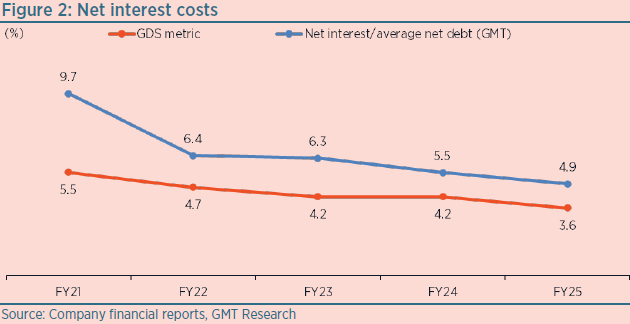

Interest costs are another area where GDS’ presentation flatters the picture. GDS discloses an effective interest rate in its results presentation, but the calculation appears problematic. It divides net interest costs by gross debt. This mixes a numerator that benefits from interest income with a denominator that excludes cash. In addition, some interest is capitalised and therefore does not flow through the income statement immediately. In FY25, using net interest cost, including capitalised interest, divided by average net debt, we estimate an effective interest rate of 4.9%, well above the 3.6% disclosed by the company, as shown in Figure 2.

This matters because the whole debate turns on the gap between asset returns and funding costs. If the business is earning only around 3% pre-tax on operating assets, while the true cost of debt is closer to 5%, then growth is not automatically value-accretive. Additional investment could compound the problem unless returns improve materially.

If returns are less than funding costs, growth is not automatically value-accretive

GDS has separated out DayOne, its international data centre platform, which may add further value if it eventually lists. However, while any listing may provide a windfall for investors, it says little about the outlook for the core China assets.

GDS reported FY25 results and FY26 guidance that were broadly in line with expectations. The concern is more fundamental: this remains a capital-heavy business generating low economic returns on a large asset base. Management’s preferred non-GAAP yield makes the portfolio look much healthier than it appears under a more credible return-on-assets approach. Depreciation, impairments, right-of-use assets, goodwill and capitalised interest are not small details. They are central to understanding the economics.

For investors, the key question is not whether demand for data centres will keep growing. It probably will. The question is whether GDS can turn that demand into returns that comfortably exceed the cost of capital. At the moment, the answer is not obvious.

[1] Some others which hit the headlines include BJ Ent Water (371 HK), Anta (2020 HK), BYD (1211 HK), China Feihe (6186 HK)

[2] Some of which include MOG Digitech (1942 HK), China Greenland BG (1253 HK), Ever Sunshine (1995 HK), Weimob (2013 HK), GSX Techedu (delisted). Apologies, but you won’t be able to access most of the research as it was written for our institutional clients and is password protected.