What is Celltrion?

Celltrion is a Korean pharmaceuticals company that develops and manufactures biosimilar drugs. These are copies of original biologic drugs on which the patents have expired. Celltrion has produced biosimilars of some of the best-selling biologics. Its most successful drug is Remsima, a copy of Remicade, one of Johnson & Johnson’s biggest drugs. It also recently received European regulatory approval for Truxima and Herzuma which are biosimilars of Rituxan and Herceptin, respectively, two of Roche’s bestselling drugs. However, Herzuma, in particular, suffered from significant delays; Celltrion originally planned to bring it to market six years ago, in 2012. Unlike Remsima, neither of these drugs has a first-mover advantage. Other drugs in Celltrion’s pipeline are likely to come to market well after competing biosimilars. Any first-mover advantage that Celltrion may have benefitted from historically, it will not enjoy with these products.

Artificial corporate structure has inflated profits

All of Celltrion’s products are marketed exclusively through its separately listed sister company, Celltrion Healthcare (091990 KS). Since 2010, sales to Healthcare have accounted for 98% of Celltrion’s revenue, excluding its Korean distributor subsidiary, Celltrion Pharm (068760 KS). This exceeds the level of related party transactions in previous accounting scandals, such as Hanergy (566 HK) and Silverlake (SILV SP).

Healthcare is an artificial entity through which Celltrion’s drugs pass on to their way to third-party regional distributors. It has few assets other than inventories, and only employs around 100 people. We suspect this structure was originally established so that Celltrion could recognise revenue and profits for drugs before they had received regulatory approval, even though there was no guarantee they would gain approval and no certainty of end-market demand. The economic substance of these sales is, therefore, highly questionable.

Celltrion continues to inflate sales and profits by selling more drugs to Healthcare than is justified by end-market demand. We estimate Celltrion’s sales to Healthcare exceeded the latter’s sales to third parties by around 20% in 2017. Unsold drugs continue to accumulate as inventory on Healthcare’s balance sheet.

Risk of huge write-down of unsold and expired inventory

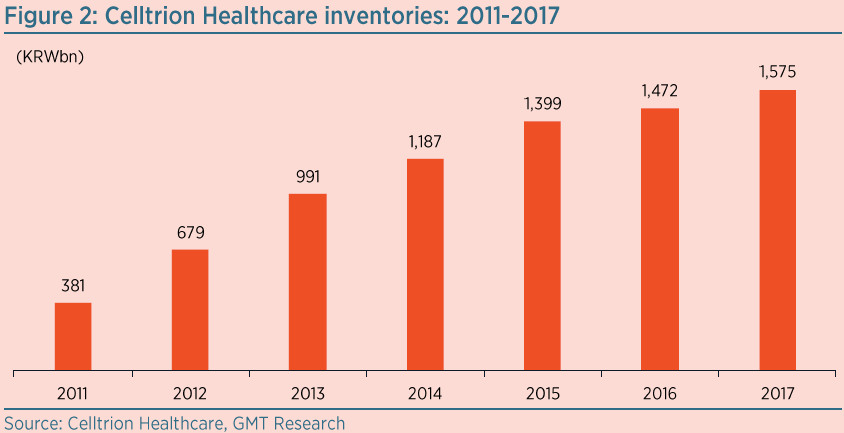

Healthcare has been unable to sell around half of all the drugs it has bought from Celltrion since 2010. Its inventory reached a staggering KRW1.6trn (US$1.5bn) at YE17, as Figure 2 shows, equal to around 2½ years of sales at the current rate. Its inventory relative to revenue is much higher than any other major pharma company.

European regulatory filings indicate that Herzuma has a shelf-life of just three years, while for Remsima it is only five years. We suspect Healthcare has held some of its inventory since at least 2010, raising concerns that much of it has expired and should have been written off; yet, so far, none has been. It would not surprise us if Healthcare had to write off KRW1trn (US$1bn) of its inventory.

Between 2010 and 2012, Healthcare sold stocks of Herzuma and Remsima on to Celltrion Pharm, a separately listed subsidiary of Celltrion, which has the exclusive marketing rights to the drugs in Korea. Pharm has not sold all of this initial inventory and has bought no further stocks of either drug, since May 2010 for Herzuma and 2012 for Remsima. The remaining inventory of Herzuma is now around eight years old, while the unsold Remsima is at least five years old. We assume Pharm is not selling out-of-date drugs in Korea, which raises doubts about whether this inventory actually exists.

Unusual accounting to inflate profits further

The auditors of the various Celltrion companies have helped them flatter their financials through the use of unusual accounting. Moreover, the three listed Celltrion companies are audited by different firms. This, in our view, greatly increases the risk that any irregularities go undetected. While it is impossible to draw any definitive conclusions from this, it certainly appears strange.

The inevitable uncertainty surrounding drug development means that almost all pharmaceutical companies expense their drug development costs. In contrast, Celltrion capitalises around three-quarters of its development expenditure. The only other pharmaceutical company we could find globally that capitalises a significant proportion of these costs is Celltrion’s Korean rival, Samsung Biologics (207940 KS), which is currently under investigation for other accounting irregularities. We estimate Celltrion overstated pre-tax profit by around 27% in 2017 by capitalising development costs, rather than expensing them in line with market practice.

Long delays to the launch of Herzuma and Celltrion’s other drugs illustrate the inherent risks in developing biologics. However, despite these delays, Celltrion has, to date, made no significant impairment charges on its capitalised development costs.

Moreover, pharmaceutical companies usually make provisions against inventory for drugs that have not yet received regulatory approval, as until then, they have zero commercial value. The amounts are written back only if the drugs are approved. Healthcare held all the inventory acquired from Celltrion at full value, even before the biosimilars were approved. We wonder how Healthcare’s auditor Samjong KPMG allowed this.

Limited competitive advantage

Remsima was fully launched in Europe in 2015, well before any other competing biosimilars, and has since taken around 50% of the market, albeit by offering hefty discounts to government purchasers. However, US sales have disappointed since it was launched there in 2016.

The success of Celltrion’s Remsima in Europe has been largely due to its first-mover advantage: it was launched several years before any other biosimilar for Remicade. This is not the case with Celltrion’s two other approved drugs, Truxima and Herzuma, where there are already competing biosimilars. As more biosimilars are launched, competition will only intensify.

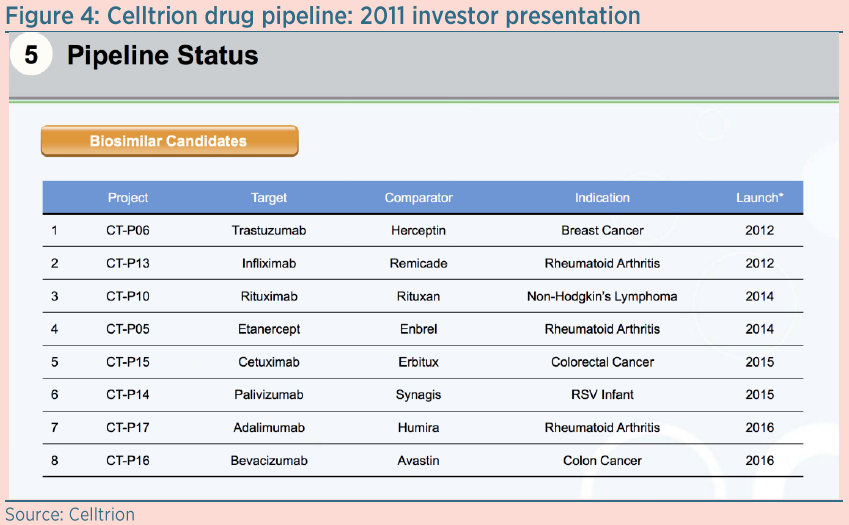

Celltrion had planned to launch five other drugs by the end of 2016, as can be seen from the slide shown in Figure 4, which is taken from a 2011 investor presentation. To date, none of these drugs have been approved, although biosimilars from other companies for Enbrel, Humira and Avastin have already received approval in the US and Europe. It is unclear why Celltrion has failed to get approval for its drugs. Moreover, even if it does eventually bring them to market, we think they will struggle to gain traction and be forced to compete on price alone.

Future demand uncertain

Healthcare has recorded impressive sales growth in recent years. Until 2017, its revenue came almost entirely from sales of Remsima. However, Remsima’s sales declined 30% in 2017, as Figure 5 shows. The shortfall was made up by a big increase in revenue from Truxima, which gained European regulatory approval in 2017. Healthcare’s sales of Truxima were particularly high in 4Q17 which may be a one off to fill distribution channels.

We think sales of Remsima may be close to their peak and may even start to fall as new competitors enter the market. Remsima already has a 50% market share in Europe, suggesting further gains in that region are likely to be limited. In the US, Remsima has so far failed gain significant market share.

We suspect distributors’ inventory levels for Remsima are high, particularly in the US. This could explain the decline in sales of Remsima in 2017 and the more than halving of Healthcare’s overall sales in the US during the year. To date, Healthcare’s US sales (almost entirely Remsima) have vastly exceeded end-market demand there; it is likely to take some time to clear this backlog. We also wonder whether sales of Truxima are sustainable at current levels and will follow a similar pattern.

Risks rising

Celltrion clearly has a genuine business: Remsima has undoubtedly been a success in the European market. However, Celltrion continues to give a misleading impression of its revenue and profits. Despite numerous attempts to contact the company with questions, we have had no response from them.