What does it do?

Sinopharm derives over 90% of its operating profits from pharmaceutical drug distribution. This is a low margin business with operating margins across the sector typically of around 4% and modest returns on capital employed of 8-11%, as shown in the charts below. There are no barriers to entry beyond, perhaps, scale. In general, margins rise as the distributor improves credit terms, and fall when credit terms are tightened.

Appearances can be deceiving

Sinopharm’s top line is expected to grow by around 10% in FY17, with bottom line growth of 12%. Meanwhile, operating cash flows have historically exceeded net profit (suggesting there are no working capital issues) while a 30% dividend pay-out ratio has been funded from reported free cash inflows. Net debt to equity of 18% by YE16 appeared comfortable and looked set to fall given free cash inflows. On 16x 2017 PER, valuations look reasonable given growth prospects and a sound balance sheet. There are 10 Buy recommendations on the stock with no Sells.

At face value, Sinopharm appears to be a solid, conservatively run business with sound financials. Unfortunately, this is largely an illusion. Our interpretation of Sinopharm’s financial position is that it is highly indebted owing to substantial operating and free cash outflows over the past five years, masked by aggressive window dressing of its balance sheet and, in our opinion, misrepresentation of its cash flow statement. So how does it do this?

Gimmick No 1: Bogus accounting

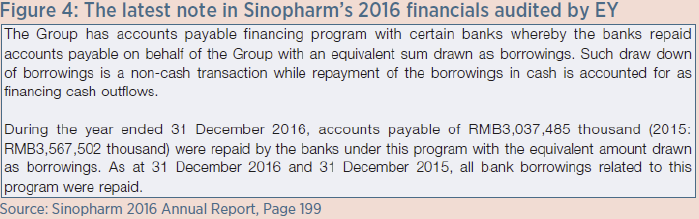

Back in 2012, Sinopharm somehow persuaded its auditors, PwC, to reclassify trade creditor repayments from an operating to a financing activity. The auditors may have been somewhat nervous about this and included a very unusual note in the payables section of its financial statements, as shown in Figure 3 which is an extract from Sinopharm’s 2012 annual report…

In 2016, EY took over the audit as part of an apparently standard auditor rotation and continued to allow this practice…

Sinopharm appears to be arguing that because its banks are repaying its trade creditors directly, these repayments should, in effect, be regarded as a financing, not an operating activity. Normally, the sale of goods from suppliers creates operating cash inflows, while repaying them create outflows. By reclassifying some creditor repayments in this way, Sinopharm has materially flattered its operating cash flows. As a result, the change in payables and debt in the cash flow statement do not reconcile with the change reported on the balance sheet.

Sinopharm appears to be arguing that because its banks are repaying its trade creditors directly, these repayments should, in effect, be regarded as a financing, not an operating activity. Normally, the sale of goods from suppliers creates operating cash inflows, while repaying them create outflows. By reclassifying some creditor repayments in this way, Sinopharm has materially flattered its operating cash flows. As a result, the change in payables and debt in the cash flow statement do not reconcile with the change reported on the balance sheet.

What we find highly unusual about this interpretation is that it would seem to contradict PwC’s own guidelines, which are based on the SEC’s position (the US securities regulator). In a November 2015 circular entitled, “Structured payables - could they be debt?”, PwC makes it quite clear that where such arrangements exist with a bank, there should be an operating cash outflow to reflect trade creditor repayments, as shown in the following extract…

Although this relates to US GAAP, it is highly likely that International Accounting Standards follow a similar interpretation. Indeed, while we have come across other instances of banks repaying creditors directly, such as Carillon (CLLN LN) in the UK, we have yet to find a company that reclassifies creditor repayments as a financing activity, including Sinopharm’s peers. This interpretation is highly questionable, being reminiscent of past accounting scandals at DHH Holdings (ENRQ US). We submitted a complaint through EY’s ethics hotline on the 4th September but it has failed to respond within its declared five working day response time. It is, once again, another indication of declining audit standards in Hong Kong.

Although this relates to US GAAP, it is highly likely that International Accounting Standards follow a similar interpretation. Indeed, while we have come across other instances of banks repaying creditors directly, such as Carillon (CLLN LN) in the UK, we have yet to find a company that reclassifies creditor repayments as a financing activity, including Sinopharm’s peers. This interpretation is highly questionable, being reminiscent of past accounting scandals at DHH Holdings (ENRQ US). We submitted a complaint through EY’s ethics hotline on the 4th September but it has failed to respond within its declared five working day response time. It is, once again, another indication of declining audit standards in Hong Kong.

The amounts are huge with around RMB22bn having been reclassified in this way between 2012 and 2016, as shown in Figure 6, representing 75% of Sinopharm’s total reported operating cash flow over this period and 139% of net profit. A further RMB1.4bn was reclassified in 1H17.

Gimmick No 2: Selling receivables

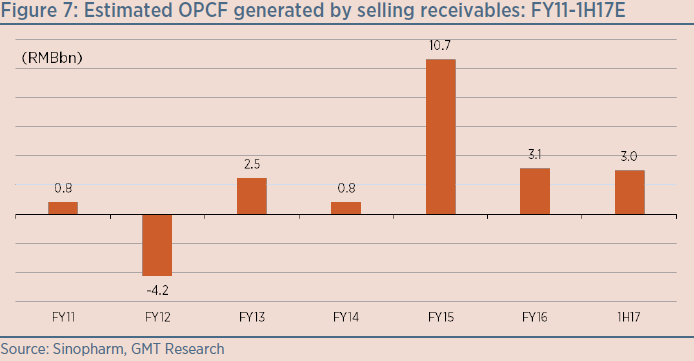

Another way to generate operating cash flows is to sell an increasing amount of receivables at period-ends. We don’t have an issue with companies that have a sensible factoring programme, especially when customers have better credit terms than themselves. By factoring the receivables of these customers, a company can lower its overall credit costs. However, we take issue with companies, such as Sinopharm, that appear to be factoring an increasing amount of receivables to create the illusion of sustainable operating cash inflows. Furthermore, the change of auditor from EY to PwC has resulted in Sinopharm no longer disclosing the amounts being factored which we have had to estimate since 2016 from the costs of factoring (the company has never disclosed amounts being discounted). Auditors are supposed to help shareholders understand the financial statements, not abet management in obscuring them.

Sinopharm’s disclosure is patchy but receivables sold rose from an estimated 13% of the total at YE12, to 24% by YE16, possibly generating a further RMB13bn of operating cash flows over this period. Interest costs associated with the selling of receivables rose by 23% YoY in 1H17. Assuming the relationship between interest costs and amounts sold remained the same, this suggests a further RMB2-4bn of operating cash inflows were generated in 1H17, as shown in Figure 7.

The reality is very different from reported numbers

If we adjust Sinopharm’s financials for the reclassification of trade creditor repayments and sale of receivables, the picture looks very different from that presented in the reported numbers. Instead of generating cumulative operating cash inflows of RMB37bn between FY12 and FY16, the company would have reported outflows of RMB6bn, as shown in Figure 8.

If we add back estimated amounts of receivables sold (factored and discounted), debtors outstanding rise from 96 days to 131 in FY16, as shown in Figure 9. Not only that, but instead of giving the appearance of an improving trend since FY14, the adjusted numbers show a deteriorating trend. Likewise, if we add receivables sold to net debt (it is, after all, a form of off-balance sheet financing), net debt to equity rises from a reported 18% by YE16, to 69%, as shown in Figure 10. Instead of appearing to be a lowly leveraged company able to pay dividends from free cash inflows, Sinopharm is a highly indebted company unable to generate operating cash inflows which is borrowing to pay dividends. Investors would likely be less willing to pay 16x 2017 PER for this latter reality.

Spicing up 1H17 numbers

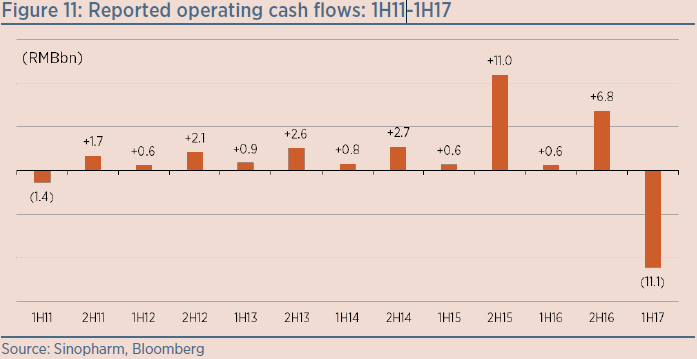

Earlier on we explained that that drug distributors’ only competitive advantage was to extend credit terms to customers. We think Sinopharm has attempted to spice up its 1H17 numbers in advance of a planned capital increase. Indeed, analysts seemed enthralled with 1H17 results which saw 9% top line growth YoY and 13% bottom line growth owing to a 15bp operating margin improvement. However, you have to look beyond the income statement to understand what was really going on. Receivables grew 20% YoY, far in excess of sales growth. This resulted in reported operating cash outflows of RMB11.1bn in 1H17. This is the largest operating cash outflow Sinopharm has ever recorded, as Figure 11 shows.

As with many other Hong Kong listed companies, Sinopharm does not produce cash flows for preliminary interim results. To find the disclosure, analysts would have needed to read through to Page 29 of the initial release, as shown below…

But there’s more

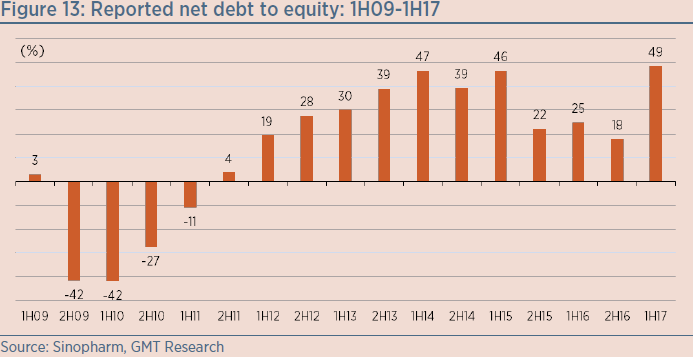

Unfortunately, operating cash outflows in 1H17 were, in reality, even larger; we estimate somewhere in excess of RMB15bn, at least RMB4bn more than reported. As discussed earlier, Sinopharm reclassified RMB1.4bn of supplier repayments as financing activities plus roughly RMB3bn of operating cash inflows raised from the accelerated sale of receivables. This explains why net debt rose by a staggering RMB15bn during 1H17. As a result, reported net debt to equity jumped from 18% at end-2016, to 49% by end-June. As Figure 13 shows, the company has never recorded such a high level of gearing or experienced such a large deterioration in such a short time. However, add back receivables sold and net debt to equity rises to 97%. That’s a lot of leverage for a company unable to generate operating cash inflows.

Over-leveraged and in need to capital

We think a capital increase may be planned, especially if creditors finally work out what’s going on with the financials. Either that, or interest expenses will begin to rise rapidly offsetting what little operating profit growth there is to be had. This perhaps explains why 1H17 results look like they had been spiced up. Worryingly, none of the sellside reports we have read highlights any of these cash flow or balance sheet issues. Maybe they don’t read beyond the income statement?

Figure 14: Watch our video on Sinopharm

Reference:

[1] SEC: SEC Charges Delphi Corporation and Nine Individuals, Including Former CEO, CFO, Treasurer and Controller, in Wide-Ranging Financial Fraud; Four Others Charged With Aiding and Abetting Related Violations, 30 Oct 2006

[2] Investopedia: What was the Mahonia company and why did it become the subject of a lawsuit?