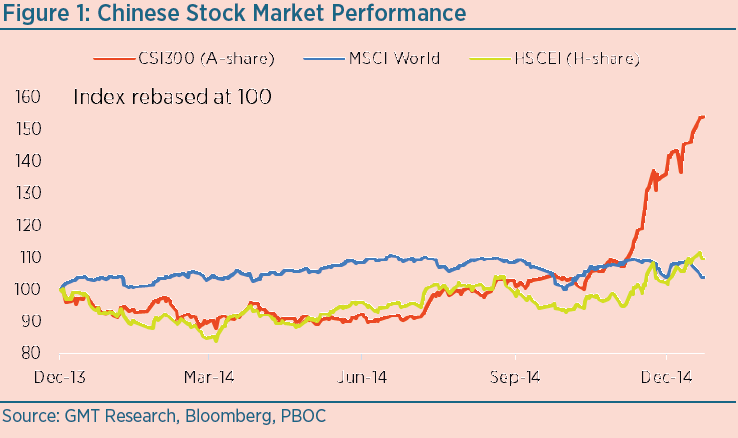

A divergence between fundamentals and equities

Sadly, we think not. While the stock market soars, Chinese corporate profits are doing the opposite. Industrial Enterprise Profits fell by 4.2% in November, the largest fall since the profit scare of 2012. Why the decline? Well, Chinese corporates are worryingly over-leveraged with debt/OPCF likely coming in at 9-10x for 2014, if our preliminary numbers are correct. This means that if capex is taken to zero, it will still take the corporate sector close to a decade to pay off its debt. The global average over the past 20 years is just 3x. In other words, the Chinese corporate sector is largely insolvent.

Beginning to cut capex

Companies are also hemorrhaging free cash outflows because capex remains too high (and this needs to be debt financed, hence rising leverage). What we are beginning to see is capex being cut in order to generate free cash inflows and de-leverage. Whilst this is very positive longer-term, in the medium-term it means lower profits and unfortunately there’s a long way to go before balance sheets are repaired. (One company’s capex is another one’s revenues and so when capex is cut, the profit pool temporarily shrinks. This is more commonly known as a recession.)

Bubble beginning to deflate

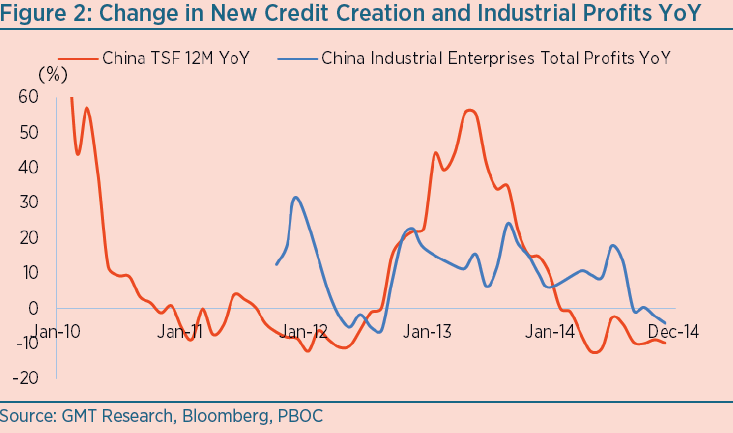

We know that companies are beginning to cut capex because quarterly results reveal this – but only slightly so far (cc-5%). We can also see that net new credit created (Total Societal Funding, “TSF”) is beginning to contract, falling by 10% in the year to November YoY (see chart below). Given that new credit is mostly used to fund capex, this decline re-confirms our view that capex is being cut. Unless the Chinese government decides to embark on another round of credit stimulus (which would ultimately be counter-productive), the bubble looks like it is beginning to deflate. After all, bubbles are only maintained by creating ever greater quantities of net new credit.

Equities: The least worst option?

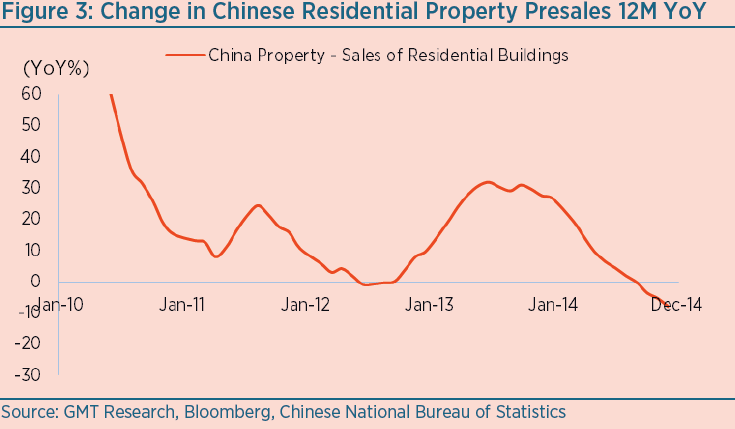

Surely, given all of this bad news the stock market should be falling? In time, it will do but although new credit is beginning to decline, China still created US$2.6trn in new money over the past year which is in the region of 28% of GDP. To put in perspective, the US only managed to generate net new credit equating to 21% of GDP in the run up to the Global Financial Crisis - and even then for just one year. Before 2014, China managed to generate net new credit in excess of 35% of GDP for five years. In other words, China’s economy is still awash with cheap money and it is looking for returns. With a crackdown in grey market financing, meagre returns from bank deposits, falling property prices (see the presales chart below), greater restrictions on the Macau casinos and capital controls remaining in place, there are limited outlets for domestic investors. The stock market had been stuck in a bear market for the better part of seven years and at face value looked cheap. To many it might have seemed the least bad investment option.

Irrational parabolic spike

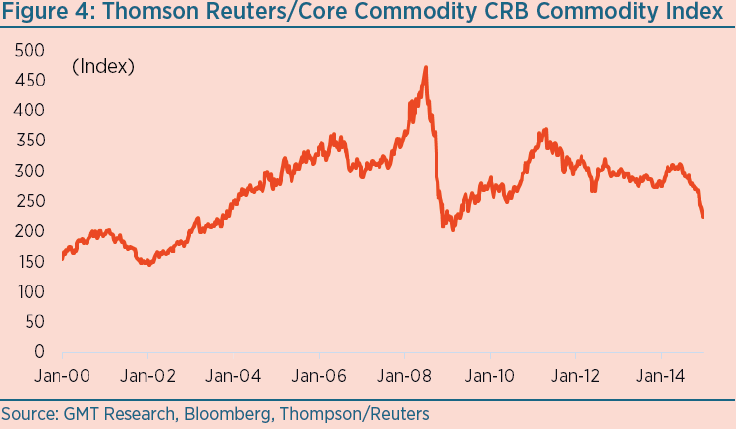

This is not the first time we have seen markets undergo seemingly irrational parabolic spikes. The Thompson Reuters Commodity Index (CRY Index, see chart below) rose almost 60% in the year to July 2008, just it was becoming clear that the global economy was entering a recession and demand for commodities would fall. Again, too much liquidity was chasing too few assets. It then more than halved over the next year as reality set in. Chinese equities have a habit of being similarly irrational. The Chinese Enterprises Index spiked by 60% as the Asian crisis unfolded in July 1997 only to collapse by 85% over the next year. This divergence today between stock market performance and economic fundamentals seems to be a repeat of the past. Chinese equities will not ignore fundamentals for much longer.

The world's most expensive stock market

It is often cited in the financial press that Chinese equities are cheap. Even before this rally, we disagreed. The main Chinese A-share equities index, the CSI300, now trades on 16x 12-month trailing PER which is broadly in line with other Asian indices. But this includes large state-owned banks which are failing to reports NPLs properly. These are some of the largest listed companies in the world and the index is heavily skewed towards them. If we use a median PER instead, the market trades on 31x PER, rising to 41x on a 5% trimmed mean basis. This arguably makes it the most expensive major equities index in the world. This might be excusable if the index was anticipating a major earnings recovery but it's not. Profits are beginning to fall and will fall even further if companies continue to cut capex.

The bubble is beginning to deflate

With fundamentals being thrown out the window, now’s probably the time to follow the chartists. Still, we would be getting our shorts ready. What makes China's stock market so terrifyingly expensive is that its economy is still in the latter throes of a bubble. Steel, cement, property and construction companies may all be trading at valuation discounts to their global peers but when the bubble bursts they will be loss-making. After all, they’re running out of “stuff” to build. As a consequence of rehousing a third of its population over the past decade, China now consumes 49% of the world’s steel and 59% of its cement. All this from a country which commands just 11% of the world’s economy and 19% of its population. In other words, it’s just not sustainable.